First Community Financial Group, Inc. Blog |

Insurance pointers and timely information at your fingertips.

Do you remember when you were young and had to check under your bed for monsters before you could go to sleep? I sure do! Because of my hyperactive imagination and the poor decision to watch one too many cheesy 80's horror movies, I was absolutely terrified of monsters when I was a kid. Every night I would thoroughly inspect all of the best hiding places in my room before I reluctantly switched off the light and frantically dashed for my bed, fully expecting to be ambushed by a mob of gremlins as soon as everything was dark. I certainly didn't want any mischievous little critters to snack on one of my exposed limbs as I slept, so I wrapped myself in a cocoon of blankets as an extra precaution. The slightest noise would make my heart race with fear and my mind travel to nightmarish situations. Peace of mind wouldn't arrive until I had finally drifted off to sleep.

Now that I am an adult who is fairly confident that there are no monsters under my bed, I have a more important question to ask: What's lurking below your mobile home? The answer probably isn't monsters, but here are three things that you may find: Animals Mice, raccoons, squirrels, skunks, insects and other critters may invade the space below your mobile home and cause messes, loud noises, bothersome odors and other damages. Keeping your trash and recycle bins tightly closed and making a point to keep the underside of your home clean of trash and debris are good strategies for keeping otherwise curious animals away. It also helps to keep bird feeders a good distance from your home, as they attract pesky squirrels and raccoons. According to SFGate, sprinkling chili or habanero flakes in the dirt around your home is an effective way to repel many animals. But if you do end up finding an animal under your home, don't try to remove it yourself. Instead, call your local animal control service−they can help you find a safe solution. Water If there is an abundance of clay in the soil around your home or if your yard is not graded well, any water that collects under your home may not be able to drain properly. Rainfall and even plumbing leaks can lead to excess moisture, and if you don't act quickly to fix this problem, your home could become musty and moldy. My Mobile Home Makeover suggests addressing the issue of pooling rain water by stapling plastic sheeting to the bottom frames of skirting so that any water that collects will be absorbed beneath the plastic and will not damage the bottom of your home. You can also install gutters to prevent rain water from pooling underneath or around your home. Holes It never hurts to thoroughly inspect the bottom of your mobile home for holes. Gaps, tears and open spaces enable animals to sneak in and make your home their own. Holes could also expose water pipes and wires, which could easily be damaged by outside elements. If you find holes in the polyethylene belly wrap below your home, SFGate suggests stuffing fiberglass insulation into the space before patching it. Additionally, cleaning the area around the hole will make the patch stick more effectively. Lastly, if you plan to file a claim with your insurance company, be sure to take photos of the holes and other damages and keep careful records of your receipts and invoices related to any mobile home underbelly repairing projects. Routinely checking under your mobile home for animals, water and holes will help you stay aware of potentially monstrous damages that require your attention. Content Provided by: Foremost Insurance Group

0 Comments

Whether you are buying your first home or moving to a new home, you have to make sure that your homeowners insurance needs are met. Homeowners insurance isn’t always easy to understand, and it does have its fair share of unique terms. It is sometimes easy to make mistakes when setting up your policy, and this might affect how much money you are entitled to receive from a settlement.

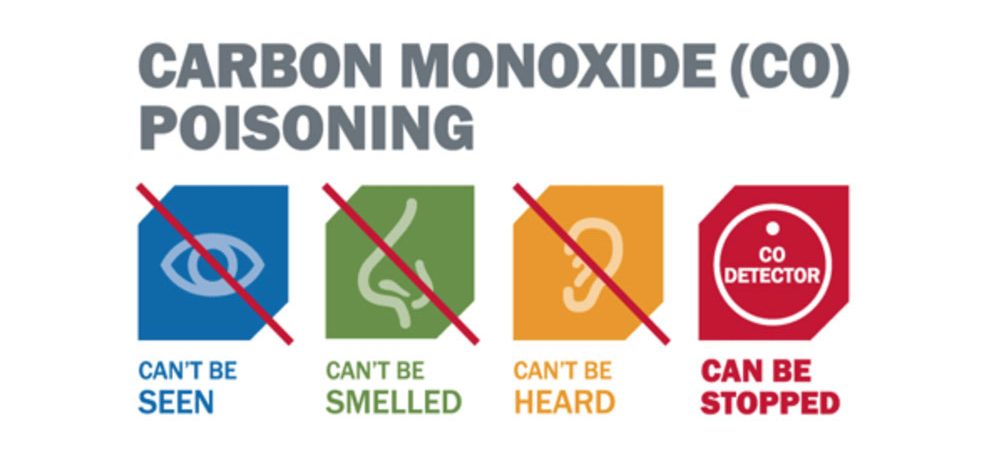

Try to avoid making the following mistakes when putting together your homeowners insurance policy. Overestimating How Much Home Insurance You Have It’s common for homebuyers to only purchase a basic homeowners insurance policy and expect it to cover them against any potential property loss. However, the most standard coverage won’t always cover you. In general, your dwelling insurance limits should be worth at least 80% of your home’s replacement cost value. Should your home be destroyed in a catastrophic event, then this coverage can help you rebuild your home similar to how it was before the hazard. Keep in mind, certain types of damage, such as earthquake and flood damage, will not be covered under your standard dwelling insurance. Waiting Too Long to File a Claim If you ever have to file a claim on your homeowners insurance, then you need to do so promptly. If you wait months (or even years) then your insurer will have a harder time verifying your claim, and as a result, they might decline to cover you. Most filing periods cut off from 30 to 90 days past the loss occurrence. The earlier you file, the sooner you will get a settlement for your losses. Having a Deductible that is Too High or Too Low Your dwelling and possessions coverage will likely contain deductibles, which are dollar amounts that you must pay for losses before your insurance will pay. So, if you have a $500 possessions deductible, then you must pay for $500 worth of damage to your possessions out of pocket before insurance will cover any damages. A deductible that is too high can make it difficult to pay when you need to. On the other hand, a deductible that is too low can result in high premiums. Not Notifying Your Insurer of Changes When you make changes in your home, you must notify your home insurer. For example, if you add a new wing to the home, then you must notify your insurer. This will guarantee that your policy will provide the appropriate coverage. Failing to notify the insurer could result in a lack of coverage later on. Don’t forget, while it is important to save money on home insurance, it is also important that you consider other aspects of coverage. It’s imperative to have the right balance of coverage, rather than the cheapest policy altogether. Our agents will help you ensure that you always have the perfect balance of coverage.  Protect your family from the ‘silent killer’Carbon monoxide is an odorless, colorless, invisible gas that results when certain fuels do not burn completely. And it can be deadly. That’s why it’s important to know how to prevent it, detect it, and protect yourself and your family from its effects. In the home, carbon monoxide is most commonly formed by flames and heaters, as well as vehicles or generators that are running in an attached garage. As temperatures drop and more people are cranking the heat and hovering over the stove inside and warming up the car’s engine before hitting the road, it’s especially critical to ensure your family’s safety against this lethal gas. Since carbon monoxide cannot be detected without a carbon monoxide detection device, it is essential to install and maintain one or more detectors in your home. Detector Tips At First Community Financial Group, we want you and your family to stay protected, so check out the following tips from CAL FIRE San Diego County Fire Authority for safeguarding your household. · The International Association of Fire Chiefs recommends a carbon monoxide detector on every floor of your home, including the basement. A detector should be located within 10 feet of each bedroom door, and there should be one near or over any attached garage. · Each detector should be replaced every five to six years. · Battery-only carbon monoxide detectors tend to go through batteries more frequently than expected. Plug-in detectors with a battery backup (for use if power is interrupted) provide less battery-changing maintenance. · Thoroughly read the installation manual that comes with the individual detector you purchase. Manufacturers’ recommendations differ to a certain degree based on research conducted with detectors for specific brands. · Remember that carbon monoxide detectors do not serve as smoke detectors and vice versa. You can, however, purchase a dual smoke/carbon monoxide detector that can perform both functions. · Do not install carbon monoxide detectors next to fuel-burning appliances, as these appliances may emit a small amount of carbon monoxide upon startup. In case of exposure At First Community Financial Group, we hope you never have to use the following tips from the Mayo Clinic, but please read on for good information that could help save a life. If you suspect that you or someone you know has been exposed to carbon monoxide, check for the following symptoms: · dull headache · weakness · dizziness · nausea · vomiting · shortness of breath · confusion · loss of consciousness If any of the symptoms exist, move the individual into fresh air and seek emergency medical care immediately. REMEMBER TO CALL 911! The CDC also has a slew of resources: Frequently Asked Questions | CDC Emergencies and Generators | CDC Prevention Guidance | Carbon Monoxide Poisoning | CDC  Every year during the holidays, people in Texas and the rest of the U.S.A. look for ways to give gifts, not just to family and friends but to those less fortunate. It’s the spirit of the season.

Unfortunately, some of the charities out there don’t help people as fully as they claim – or possibly not at all. As if that weren’t enough, bogus organizations take advantage of people’s goodwill by stealing credit card and bank account information, along with identities, from people who think they’re donating to a legitimate cause. It doesn’t mean you can’t be generous this holiday season. It just means a little extra caution is in order. Here are four tips for making smart and safe holiday donations: 1. Verify the charity is legitimate. Sure, the name sounds official and you think your friend mentioned what good work they do. Or does the charity simply have a name similar to another well-known organization? Before you donate, do a little digging. Enter the charity’s name at Better Business Bureau, Charity Navigator or GuideStar, and, if you feel comfortable after reading about the organization, go ahead and donate. If not, look for another charity that supports the same cause. A good rule of thumb is to look for organizations with 501(c)(3) status. 2. Steer clear of pop-up charities. A pop-up charity is anything but charitable. These groups spring into action at opportune times, namely when people are feeling generous, such as during the holidays or following a disaster. The so-called charity is actually a scam designed to steal money, credit card numbers, bank account information and identities from unsuspecting donors. If, during your research, you come across an organization that seemingly appeared out of the blue, do not share any of your personal information with it. 3. Be careful with digital donations. Now that you’ve researched the charity, how do you plan to donate? If it’s online, be sure to type in the website address correctly. Fraudsters put up realistic-looking sites using a URL similar to a well-known charity’s to trick people into donating. But, they’re not donating at all. They’re lining the pockets of thieves. Once you know you’re on the correct site, check that it’s secure before submitting any credit card information. Simply look for “https” instead of “http” at the beginning of the URL. Likewise, that email you received from a prominent charity may be a fake. Instead of clicking on a link in an email to donate, go directly to your Web browser and type in the address yourself. 4. Avoid phone and door-to-door solicitors. If people call or knock on your door out of the blue asking for a contribution to this or that organization, ask them for the charity’s website or mailing address instead of donating right then and there. Even if it’s a charity you’ve heard of, the operation may be a scam. It’s always safer for you to initiate the donation by visiting the charity’s website or mailing in a check. Plus, fundraising over the phone requires a middleman – that agent calling you – who must be paid, reducing the amount of your donation that goes to the charity. It feels good to be in a giving mood during the holidays. With a little legwork to look into the legitimacy and practices of the charity, your donation will help others feel good too. Contact Us! At First Community Financial Group, we can work with you to make sure you've got the coverage you need, while at the same time using all possible credits and discounts to make that coverage affordable. Just give us a call at 936-327-4364 or send us a note at info@firstcfg.com. We want to help you meet your goals, and make sure what's important to you is protected! Content provided by Safeco Insurance.  The holidays have arrived in Livingston and East Texas! For those with one or more four-legged friends in the house, it’s time to go over some safety tips. After all, you want all of your family members to enjoy the festivities – even the furry ones.

The American Society for the Prevention of Cruelty to Animals, which operates the 24-hour Animal Poison Control Center at 888-426-4435, takes calls year round about pets being exposed to potentially hazardous yet common household items. With the house filled with guests, presents and decorations during the holidays, the risks multiply. Here are some things to remember and consider from Thanksgiving through New Year’s to help keep Fluffy or Fido healthy, happy and safe: Houseguests Make sure everyone keeps medicine bottles or pill cases safely tucked away – actually that applies to everyone in your household, both permanent residents and visitors. And, just in case a probing pet gets into some medications, always make sure the containers are labeled with the contents and potency so you know what was ingested. Of course, the holidays wouldn’t be complete without sharing in feasts and treats with family and friends. Just make sure that doesn’t extend to your pets. After all, some things on the holiday dinner table, such as alcohol and chocolate, are toxic for pets. And, because all of the seasonal commotion may become too much for your pets, be sure they have a quiet place to which they can retreat. Let others know your pets shouldn’t be disturbed when they are in their quiet spot, whether it’s a bed, a cozy blanket or a kennel. Presents Those beautifully wrapped presents under the tree or covering the fireplace mantel can also be harmful to your oh-so-curious felines and canines – especially if a present contains treats for them or food for humans. Animals have a keen sense of smell and, once they sense that food is nearby, they’ll be more than happy to unwrap and eat both the outer and inner contents of the gift. Those ribbons and bows that you worked so hard on perfecting may end up wreaking havoc on your pet’s digestive tract. Decorations Besides the obvious precautions of making sure wires, batteries and poisonous/toxic plants (such as holly, mistletoe and poinsettias) are all out of paw’s reach, make sure that plastic and glass ornaments are far away as well. If chewed or eaten, these items can cause electrical shock, acid burns, dermatitis and mouth abrasions. You should also remember that, as beautiful and fun as they are, snow globes contain ethylene glycol, a highly toxic substance to all pets. Another substance that you may not think of as harmful to pets is salt, and homemade play dough is loaded with it. Watch pets while your children are playing with it or around ornaments made with it. The dough can cause life-threatening electrolyte imbalances. Scented candles may also be a holiday staple, but they may be enticing to our pets, which are at risk for serious burns and other injuries. Best to keep those candles completely out of reach. Finally, make sure you have the phone number for your local emergency veterinarian or the ASPCA hotline on hand for emergencies. With these tips in mind, you can help keep your four-legged family member safe during the holidays – and all year round. We here at First Community Financial Group wish you a very happy holiday season!  Texas' roads are full of cars — but often, they’re also full of wildlife. That’s why an estimated 2 million vehicle-animal collisions happen each year across America, according to the U.S. Department of Agriculture. Fall and winter constitute the most dangerous periods for these incidents. Visibility is reduced, thanks to the shorter days and inclement weather, and it’s also migration and mating season for many animals. But, you can still take steps to decrease the chances you’ll hit an animal. Here are five things to do: 1. Be particularly alert at dawn and dusk. Visibility is low at these times, and animal activity is high. 2. Keep an eye out for signs. If you’re in an area where wildlife is common, you may see posted warnings. 3. Watch your speed. Avoiding any kind of collision is easier if you’re travelling at an appropriate rate of speed. And, it’s not just about the speed limit. In certain conditions, driving under the speed limit is more optimal. 4. See an animal? Look for more. Missing one animal doesn’t mean you’re out of the woods, so to speak. There are probably others around. 5. Don’t swerve. If possible, don’t make any wild maneuvers. You could end up hitting something worse than an animal — like another car — or going into a ditch or down an embankment. Use your brakes, use your horn, and use your good judgment. Sometimes, though, collisions just can’t be avoided. If you do hit an animal, here’s what to do next: · Call 911 for assistance, especially if there are injuries to you or passengers. · Don’t touch the animal. They can be dangerous, even when hurt. · Document the accident scene and the damage to your car. · Get in touch with your insurance carrier or with us. Keep in mind that the same attributes that make for safe everyday driving can also help you avoid animal collisions: Remain alert, maintain a safe speed for conditions and avoid distractions. Also, be sure to carry adequate car insurance in case something – animal-related or otherwise – does happen.  Unique among motor sports, driving all-terrain vehicles in Texas combines an exhilarating workout with a test of maneuvering skills and a hearty dose of adrenaline. Fun as it is though, it can be a risky activity. So, take a systematic approach to keeping things safe before, during and after your outings. Before You Go · Take a Course Formal hands-on training courses cover how to control ATVs in commonplace situations. The ATV Safety Institute typically offers its ATV Rider Course free to anyone who buys a new qualifying machine from an institute member. Call 1-800-887-2887 or visit atvsafety.org for class information. · Dress for Success A motorcycle or other motorized sports helmet, certified by the U.S. Department of Transportation, is a must. You’ll also want to suit up with over-the-ankle boots and long pants, a long-sleeved shirt, goggles and gloves. · Remember Insurance Riding on state-owned land? Many states requireATV insurance, which offers coverage options similar to what’s available for motorcycles – liability, comprehensive, collision, safety apparel replacement, roadside assistance and more. During the Ride · Don’t Share the Seat You’ll want to be free to shift your weight according to the terrain and the situation. Passengers make it difficult – and dangerous. · Stay Off the Road ATVs simply aren't street-legal machines, at least not in most states. The solid rear axle with no differential means they can be hard to handle on pavement. · Let Kids Be Kids Children should never be allowed to drive or ride on an adult ATV. Someone under 16 on an adult ATV is twice as likely to sustain an injury as a child riding a youth ATV, according to ATVSafety.gov. After the Outing · Wait to Celebrate This is when you get to unwind with a cold one, not before. You need sharp reaction time and judgment, so don’t ever drive ATVs under the influence of alcohol or drugs. We here at First Community Financial Group want you to enjoy your ATV outings this summer, while staying safe. Just give us a ring if we can help you explore ATV insurance options!  Summer and early autumn are perfect times for sitting in the backyard, listening to the sounds of nature, watching the sunset and enjoying a campfire.

As the coolness of the evening creeps in, a campfire is a great way to keep warm and socialize. That’s especially true in today’s world of social distancing—outdoors are the safest places to socialize, and bonfires are great ways to do so. Maybe you’re even using that campfire as a cooking stove from time to time, to roast marshmallows or cook hamburgers. These all sound like great ideas, but any idea involving a bonfire or campfire is going to have its risks attached. It’s an open flame that you must control carefully, or else you will run the risk of causing a fire that might easily get out of control and do a lot of damage. In order to keep your family and property safe when building campfires, keep a few of these tips in mind:

You can make a lot of memories while sitting around a campfire. But if you don’t do so safely, you could wind up facing a lot of property damage that could be a massive strain on your insurance liabilities. That’s why it’s always better to plan ahead than to wait until it is too late. If you’re looking to buy a homeowners insurance policy that is perfect for your needs, just call our agency today. We’re here to help you get a customized, affordable policy portfolio no matter what you need.  Your business would not be able to succeed if the equipment, materials, stock and products that it utilizes were to become compromised. Damage, theft or destruction of property might interrupt your operations and put you in a significant financial bind as you work through the recovery process. Indeed, if the loss of property is too great to bear, then the business might fold.

If you are committed to bracing your business against this threat, then you should consider commercial property insurance to be indispensable. This benefit might be required in some circumstances, but it’s critical to have in all cases. Any business that owns property—which is more or less any business—can benefit from this plan. What Does Commercial Property Insurance Cover? A commercial property policy is designed to help you repair assets damaged by unexpected, unavoidable accidents that impact your operations. It might apply to losses stemming from:

This insurance may cover the physical location and all of its contents including decorations, furniture, equipment, products and more. Make sure to speak with your insurance agent to ensure that your business’ valuable assets are covered appropriately. Do You Need Commercial Property Insurance Without a Physical Location? The days of the brick-and-mortar business are over, and today you can run a successful enterprise even from the comfort of your own home. However, commercial property insurance remains essential for your operational needs. Indeed, your standard homeowners insurance will not cover commercial property except in very limited cases. Commercial property insurance can cover items specifically used for your business, whether they are housed in a physical location or in your home. There are property damage risks everywhere, and all of them could impact your operations. You can rely upon your commercial property insurance to help you cover the costs of repairing, replacing or recovering these items so that you can sustain as little of a financial loss as possible in the meantime. How do I Get the Right Commercial Property Insurance? In some cases, you will have to buy your commercial property insurance as a stand-alone plan. In others, however, this benefit will come as part of a business owners policy (BOP). BOPs provide several essential commercial benefits, including commercial property insurance, in one place. Therefore, by having your commercial property coverage as part of this plan, you’ll be able to both coordinate your benefits and pay a lower price for your coverage overall. It is never too soon to consider protecting the physical assets of your business. Keep your eyes peeled, compare quotes and speak to one of our insurance agents about protecting your business’s property with the right coverage.  Do you own a boat? If you live in Texas or near Lake Livingston, you might! Ever wonder what you should ask your agent or broker about insuring it? Brad Seeley, senior marine product manager for Foremost Insurance Company, has some suggestions:

1. Do I need insurance for my boat? "Some people may think that their boat is adequately covered through an endorsement on their homeowner's policy," explains Seeley. "Worse yet, they don't carry any coverage at all. Boat owners should look for a specialized insurance policy that offers the coverages that fit their boat and lifestyle. It's better to be prepared and have it insured for peace of mind while on the water." 2. Will my personal property be covered? "Buying life vests, water skis and fishing gear can really add up," says Seeley. "A good policy will not only provide coverage for all of this equipment, but also for other personal property on board." 3. What discounts are available? "There's a variety of discounts a customer could qualify for, like a multi-policy discount if they insure more than just a boat with the same company, or a multi-unit discount if they insure more than one boat," states Seeley. "Discounts will help a customer save money on the policy's premium." 4. Is Towing and Assistance available? "A day of fun in the sun could easily be ruined if the boat breaks down while on the water," adds Seeley. "This is a great coverage to add to a policy and covers either the cost of certain emergency fixes at the point where the boat broke down, or the cost of towing the boat to nearest repair shop. Towing and assistance should also apply to the trailer if it breaks down while towing the boat." 5. Is the type of boat I have eligible for insurance coverage? "There are many different kinds of boats — pontoons, open bow, fishing boats, cabin cruisers—and even more things to consider like speed, length, value and use of the vessels. " explains Seeley. "That's why it's important to make sure your agent knows all these things up front, even how you will use your boat. Your agent can help you get the coverages that are just the right fit." Your safety is number one to us. Stay safe this summer on the shore and on your boat. Contact First Community Financial Group today to get a free quote for you boat, motorcycle, ATV and more! |

Contact Us(936) 327-4364 Archives

March 2024

Categories

All

|

Navigation |

Connect With Us

Share This Page |

Contact UsFirst Community Financial Group, Inc.

115 W. Polk St. Livingston, TX 77351 (936) 327-4364 Click Here to Email Us |

Location

|

RSS Feed

RSS Feed