First Community Financial Group, Inc. Blog |

Insurance pointers and timely information at your fingertips.

|

The cost to rebuild your home is its replacement value. This can be very different from the estimated market value or actual purchase price. In most cases, it costs more to rebuild the home you own than to buy a new one.

Texas - How much home insurance is right for you? Based in Livingston, TX, First Community Financial Group understands the home insurance needs of our customers. We’ll work with you to estimate the replacement cost for your home and to adjust your policy limits from time to time as needed. It is critical that you provide us with accurate, updated information about your home and contents. If your dwelling limit accurately reflects your home’s true replacement cost, some companies will pay more than the limit if a covered loss is greater than the limit on your policy. Once a review of your home and possessions indicates you are properly insured, it’s a good idea to reexamine your coverages and limits from time to time, especially whenever you make additions or improvements. First Community Financial Group can help you re-evaluate your insurance needs, just give us a call at 936-327-4364 to speak with one of our agents. Texas - Be Sure You Have Enough Homeowners Insurance Here are some steps you can take to reduce the danger of being seriously underinsured:

Consider whether you should have more coverage for personal property (contents) than your policy provides. Personal property coverage is usually 70% of the coverage limit for the structure. Your limit may be lower than 70%. Supplemental protection is available for a small additional premium. Inventory your home. Prepare an inventory of personal property items, update it periodically, and keep it in a safe place outside your home, such as a safe deposit box at your bank. It will save you hours of time trying to list everything damaged or destroyed if you need to make a claim. It will also help ensure you don’t forget some items. First Community Financial Group can advise you on ways to simplify the job of preparing a personal property inventory such as videotaping each room with descriptive information on the sound track. Personal Liability Besides making sure you have enough protection to cover possible damage to your own home and contents, you should also evaluate your exposure to liability risks. These result from damage to the property of another, or injury to a person, not a member of your household, for which you can be responsible. In recent years it’s become common for homeowners to be sued for injuries or damages to others, even when there is no evidence of negligence by the homeowner. The reality today is if you have any appreciable assets, you are exposed to the risk of being sued. Even if you ultimately prevail in court, your legal fees and the months or years of worry and uncertainty can be a terrible burden on you and your family. The Personal Liability coverage provided by your Homeowners Policy usually provides a limit of $100,000 or $300,000. We recommend increasing this protection with a personal umbrella policy. Not only will it increase your personal liability, but also your auto liability. Limits are available from $1 million to $10 million and beyond. The cost of this coverage is usually very reasonable. Keep in mind that Texas can require certain minimum levels of coverage. The right coverage for you is unique – talk to the agents at First Community Financial Group today to find out how to get the best price and value on home insurance for you.

0 Comments

It's important to know that most home policies don't cover flooding and just a few inches of water damage can cost thousands. Even those who don't live near water are at risk, because anywhere it rains, it can flood. Heavy rains, clogged or insufficient drainage systems, nearby construction projects, broken water mains and inadequate levees and dams can cause flooding that put your Home and belongings at risk. Your home is one of your greatest investments. It's important to prepare ahead in the instance that a disaster could occur. Here are three simple steps to help make sure you're ready in the event of a Flood.

Call our agency today if you need a flood quote or have questions about your coverage! (936) 327-4364  Thinking about a DIY home improvement project? Maybe a new kitchen or bathroom makeover?

If project excites you, you’re not alone. The Home Improvement Research Institute (HIRI) says do-it-yourselfers complete two-thirds of home improvement projects — and spend less than those who depend solely on contractors. While saving money is satisfying, the sense of accomplishment DIYers feel is even better. But before you pick up a hammer or grab a paintbrush, you’ll need to do some homework. As you draw plans, budget, purchase materials and secure permits, you also need to think about insurance. Talk to your Trusted Choice Independent Insurance Agent® at First Community Financial Group before you start work. Your agent can help you assess the unexpected risks of your project. Here are five common renovation projects that may require additional insurance: Kitchen renovation Maybe you’ve been dreaming of a new kitchen, one with quartz countertops and Wi-Fi-enabled appliances. Kitchen remodels can add convenience and significant value to your home, but there are a few insurance considerations: • Depending on your level of experience, you may need the help of a plumber or electrician. Make sure the contractors you hire are bonded and insured. Do they carry liability insurance? Ask to see their certificate of coverage. • Check with your agent to see if you should increase your homeowners coverage. If your renovation substantially increases the value of your house, you could be underinsured if you haven’t raised your limits. Generally, you need enough insurance to replace 80% of your home’s value. • Will friends be helping you? Ask your agent about adding no-fault coverage or raising your medical expenses coverage. Bathroom makeover You have visions of a soaking tub, new vanities and imported marble tile. Sounds delightful, but keep these points in mind: • You may need a plumber to help you move a water line or drain. Bear in mind that water damage caused by your faulty workmanship won’t be covered by your homeowners policy. On the other hand, if you use a contractor, their business insurance should cover the damage to your home. • Will that expensive marble be sitting in your driveway after it’s delivered? Costly materials have a way of walking away from a job site. Check to see if your policy covers theft or damage to your building materials. Home office You’ve decided to convert a spare bedroom into a home office. It’s an easy renovation, but here are some insurance considerations: • Most homeowners policies only provide limited coverage (up to about $2,500) for office equipment. If you have items that exceed that amount, you’ll need additional coverage. Your agent can recommend some options. • If you’re doing work for your firm at home, make sure you’re covered by the company’s business and workers’ compensation policies. If you’re self-employed, you may need a separate business policy, especially if clients visit your house. Sunroom You’ve always wanted a room off the kitchen to take advantage of the morning sun. Sunrooms can provide enjoyment year-round, but you do need to keep a few things in mind: • Talk to your agent about adding a new room to your homeowners policy. You may be able to get a discount if you install energy-efficient windows or heavy-duty locks on an exterior door. • Is the project insured against severe weather? Theft or vandalism? You may need a builders risk policy. Finished basement You’re planning to create extra living space in the basement for your growing family. You’ve contracted to have a French drain and a sump pump installed to prevent water from leaking in. You’ve also decided to live in a friend’s house while you work on the project. Other Considerations: •If your house is unoccupied during construction, you may need vacant home insurance. • Be sure to get a warranty on the French drain. Flooding isn’t covered by homeowners insurance. However, you can add water backup coverage to your policy to pay for damage if your sump pump fails. • Game room? Home theater? Extra bathroom? You may need to increase the limits on your homeowners policy. n the other hand, upgrading old wiring or installing a security system could lower your premiums. If you’ve got the home renovation bug, maybe it’s time you joined the ranks of millions of satisfied DIYers. Just remember to contact your Trusted Choice agent at First Community Financial Group to get your insurance needs squared away. Then you can hammer to your heart’s content. When the time comes to consider which type of home insurance to buy or how much coverage you need, think twice about just renewing the coverage you currently have. In many situations, your coverage can become ineffective or provide insufficient coverage to meet your needs if a significant issue occurs on the property. Be sure to take a closer look at your home insurance plan to ensure it offers the right level of coverage for your home right now. If it doesn’t, you could face financial loss later when you have to file a claim.

To estimate your insurance needs, consider a home rebuild analysis. This will help you get an accurate idea of what it would cost to rebuild your home at today’s construction costs. Update your home insurance policy to reflect the true cost so that if an event occurs in which your home is at risk of damage, you will have the coverage available to minimize those losses. Update your home insurance policy at least once every year or so to reflect changes in construction costs. How Can You Ensure You Have Enough Coverage? Determining if there is enough homeowners coverage in place to protect against a significant loss is a considerable undertaking. If your home is impacted by fire or destroyed in a storm, for example, then the amount of damage present can warrant the need to not only replace what you’ve lost, but also to rebuild your property. That is why a home rebuild cost analysis is necessary. This type of process helps to identify the costs of rebuilding your home, not just covering its value. Rebuilding your home includes coverage for the construction process. With a home rebuild cost analysis, it becomes easy to learn what the true cost of rebuilding your home will be. Unfortunately, most people do not have enough coverage to completely rebuild their homes with no out-of-pocket expenses to them. However, with a home rebuild cost analysis, you can better calculate what that amount of money would be. It’s also important to consider the replacement value of your home versus the actual cash value. Depreciation can have a significant impact on your actual cash value claim. For example, if your siding needs to be replaced at 15 years old, but it has a 20-year lifespan, you will be expected to cover most of the roof’s cost. Replacement value, on the other hand will cover rebuilding costs, regardless of depreciation. It’s important to take all costs into consideration. Do you have enough coverage? Contact us for more information on home insurance. Whether you are buying your first home or moving to a new home, you have to make sure that your homeowners insurance needs are met. Homeowners insurance isn’t always easy to understand, and it does have its fair share of unique terms. It is sometimes easy to make mistakes when setting up your policy, and this might affect how much money you are entitled to receive from a settlement.

Try to avoid making the following mistakes when putting together your homeowners insurance policy. Overestimating How Much Home Insurance You Have It’s common for homebuyers to only purchase a basic homeowners insurance policy and expect it to cover them against any potential property loss. However, the most standard coverage won’t always cover you. In general, your dwelling insurance limits should be worth at least 80% of your home’s replacement cost value. Should your home be destroyed in a catastrophic event, then this coverage can help you rebuild your home similar to how it was before the hazard. Keep in mind, certain types of damage, such as earthquake and flood damage, will not be covered under your standard dwelling insurance. Waiting Too Long to File a Claim If you ever have to file a claim on your homeowners insurance, then you need to do so promptly. If you wait months (or even years) then your insurer will have a harder time verifying your claim, and as a result, they might decline to cover you. Most filing periods cut off from 30 to 90 days past the loss occurrence. The earlier you file, the sooner you will get a settlement for your losses. Having a Deductible that is Too High or Too Low Your dwelling and possessions coverage will likely contain deductibles, which are dollar amounts that you must pay for losses before your insurance will pay. So, if you have a $500 possessions deductible, then you must pay for $500 worth of damage to your possessions out of pocket before insurance will cover any damages. A deductible that is too high can make it difficult to pay when you need to. On the other hand, a deductible that is too low can result in high premiums. Not Notifying Your Insurer of Changes When you make changes in your home, you must notify your home insurer. For example, if you add a new wing to the home, then you must notify your insurer. This will guarantee that your policy will provide the appropriate coverage. Failing to notify the insurer could result in a lack of coverage later on. Don’t forget, while it is important to save money on home insurance, it is also important that you consider other aspects of coverage. It’s imperative to have the right balance of coverage, rather than the cheapest policy altogether. Our agents will help you ensure that you always have the perfect balance of coverage.

Anyone who's been through a flood knows that recovering after this kind of disaster isn't easy. You're forced to accept that irreplaceable family treasures and memories may be gone forever, your furniture is destroyed, potentially along with your home. It's a devastating and emotional moment and a lot to take in all at once. But you know the only thing you can do is move forward, and begin the steps needed to restore your home. As soon as the floodwaters recede, you can return to your home as long as officials give the OK to do so. Before entering your home, however, make sure it is safe! Tips for staying safe upon return:

Bring waterproof boots, a first aid kit, cleaning supplies and a battery-powered flashlight with you before entering the house! You never know what you'll run into. Tips for claim reporting: Another important step to take when recovering from a flood is reporting your loss immediately to your insurance agent or carrier. While flood coverage is typically not provided under most homeowners and renters policies, flood insurance may be available to you through the federally regulated program known as the National Flood Insurance Program (NFIP). If you need assistance to locate your flood insurance carrier, you can call 1-800-621-FEMA (3362). A claims adjuster should contact you within a day or two after report of the claim, depending on the severity of the flood event. When reporting a claim, you should have the following information available:

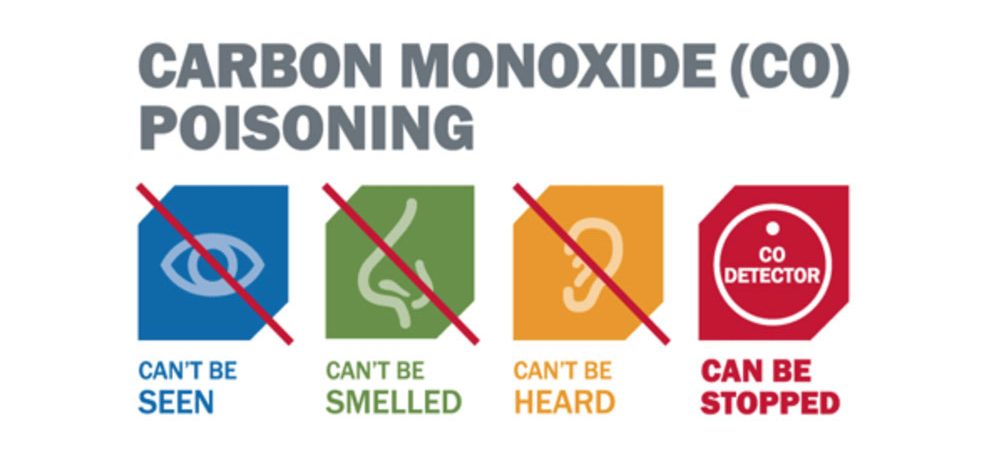

When the adjuster arrives, they will inspect your property including taking measurements and photos and give you an overview of the NFIP flood claims process. Remember that some flood insurance claims are more complex than others. Some may be opened and closed quickly, while others may take weeks or even months to resolve. If your vehicle was also damaged in a flood event, it's best to call your auto insurance provider to see if you're covered for the loss. Contact us today for a free Flood Quote.  Snow-mageddon in February 2021 hit all Texans hard. Many of our customers had losses due to frozen pipes. It’s hard to think of a worse start to a winter day in Texas than turning on the faucet and … nothing. Maybe there’s a trickle of water, but it’s clear you have a frozen pipe. So, what now? Here are some smart tips to help you prevent or address what could easily become a very messy and expensive situation: · See to your outdoor water lines: Before cold weather arrives, drain water sprinkler and swimming pool supply lines, and remove, drain and store outdoor hoses. If possible, close inside valves supplying outdoor hose bibs, and open the outside hose bibs for draining. Keep them open so any remaining water can expand without breaking the pipe. If you can't shut off the water from the inside, pick up some foam faucet covers. · Keep your home warm: Maintain an interior temperature of at least 55 degrees Fahrenheit, even when you’re sleeping or not at home. Seal any drafts and leave interior doors open to help keep an even temperature from room to room. · Tend to those pipes: Leave the cabinet doors open in the kitchen and bathroom so your pipes aren’t shut off from the warm air. You can also insulate your pipes with sleeves, heat tape or heat cable. Insulation is especially important in unheated areas, such as your attic, basement, garage or crawl space, and for pipes running along exterior walls. During severe cold spells, you may want to leave all faucets, both hot and cold, running at a slight trickle. · Call in a professional: Frozen water in your pipes can cause them to burst, meaning you’ll have a mess on your hands once that water unthaws. So, act quickly to shut off your main water supply, and call in a licensed plumber to see to the situation. Finally, be sure to touch base with us at First Community Financial Group to check whether you’re covered for the damage a frozen pipe may cause. We’re happy to answer all of your policy questions this winter, and beyond. Insurance Products - Insurance Information - FIRST COMMUNITY FINANCIAL GROUP, INC. (firstcfg.com) Report a Claim - File Insurance Claims - FIRST COMMUNITY FINANCIAL GROUP, INC. (firstcfg.com)  Protect your family from the ‘silent killer’Carbon monoxide is an odorless, colorless, invisible gas that results when certain fuels do not burn completely. And it can be deadly. That’s why it’s important to know how to prevent it, detect it, and protect yourself and your family from its effects. In the home, carbon monoxide is most commonly formed by flames and heaters, as well as vehicles or generators that are running in an attached garage. As temperatures drop and more people are cranking the heat and hovering over the stove inside and warming up the car’s engine before hitting the road, it’s especially critical to ensure your family’s safety against this lethal gas. Since carbon monoxide cannot be detected without a carbon monoxide detection device, it is essential to install and maintain one or more detectors in your home. Detector Tips At First Community Financial Group, we want you and your family to stay protected, so check out the following tips from CAL FIRE San Diego County Fire Authority for safeguarding your household. · The International Association of Fire Chiefs recommends a carbon monoxide detector on every floor of your home, including the basement. A detector should be located within 10 feet of each bedroom door, and there should be one near or over any attached garage. · Each detector should be replaced every five to six years. · Battery-only carbon monoxide detectors tend to go through batteries more frequently than expected. Plug-in detectors with a battery backup (for use if power is interrupted) provide less battery-changing maintenance. · Thoroughly read the installation manual that comes with the individual detector you purchase. Manufacturers’ recommendations differ to a certain degree based on research conducted with detectors for specific brands. · Remember that carbon monoxide detectors do not serve as smoke detectors and vice versa. You can, however, purchase a dual smoke/carbon monoxide detector that can perform both functions. · Do not install carbon monoxide detectors next to fuel-burning appliances, as these appliances may emit a small amount of carbon monoxide upon startup. In case of exposure At First Community Financial Group, we hope you never have to use the following tips from the Mayo Clinic, but please read on for good information that could help save a life. If you suspect that you or someone you know has been exposed to carbon monoxide, check for the following symptoms: · dull headache · weakness · dizziness · nausea · vomiting · shortness of breath · confusion · loss of consciousness If any of the symptoms exist, move the individual into fresh air and seek emergency medical care immediately. REMEMBER TO CALL 911! The CDC also has a slew of resources: Frequently Asked Questions | CDC Emergencies and Generators | CDC Prevention Guidance | Carbon Monoxide Poisoning | CDC  10 Things to Do to Prepare Your Home for Fall

Fall is a wonderful time in Livingston, TX and all of East Texas — if your home is ready for it. Yes, this is the time of year to fix small problems before they become big, and big ones before they become catastrophic. Here are 10 tips to help: 1. Look up. Examine your roof closely. Remove moss, clear debris from your gutters and downspouts, and repair any damage. 2. Look down. Check for signs of animals and insects around your home and garage, including in the basement and crawlspace. Bring in a professional to get rid of unwanted guests. 3. Keep things warm. Heat escapes through leaks around windows and doors, so seal up any drafty areas. Outside, put covers over faucets before temperatures drop. 4. Keep things dry. Drain outdoor hoses, faucets and irrigation systems. Look in the basement and crawlspace for wet spots. And, make sure your water heater or boiler isn’t leaking. 5. Clear the air (or vents and filters, at least). When’s the last time you checked your dryer vent? You should take a look at attic vents and exhaust ducts, as well. And, change that furnace filter! 6. Take a walk. Cracks in your driveway or walkways will only get bigger, so get them fixed soon. If your deck has signs of wear, make repairs now. 7. Get a tune-up. You or a professional should clean and tune your furnace, boiler and/or water heater, as well as your oven and range. 8. Don’t play with fire. Before building your first fireplace fire of the season, check for soot or creosote build-up. 9. Don’t play with fire extinguishers, either. But, check them to ensure they still have pressure. Don’t have fire extinguishers? Put them on your shopping list, ideally one for each floor. 10. Don’t forget those smoke and carbon-monoxide detectors. Replace batteries when needed, and test regularly that alarms are working. Keeping your home insurance policy in tip-top condition is smart, too. Remember to check in with us at least once a year to update your policy so you’re covered for your new remodel, additions or personal possessions.  I’ll start off by saying the obvious – losing power in your home in Texas is no fun. Whether it’s due to a storm, freezing weather, a short circuit or a squirrel that decides to climb up on a power line and start chewing (this happened to me one summer), losing your electricity can happen any time of the year for an abundance of reasons. If you don’t have any backup, you’ll either have to stick it out until it turns back on, go stay in a hotel or temporarily move in with friends and family. If you have a generator, it can definitely help your life go back to normal in the event of a power outage. However, because you rarely rely on them, it’s easy to overlook some basic safety measures that go along with operating a generator. Whenever you use your generator or if you decide to invest in one, keep these tips in mind to avoid carbon monoxide poisoning and other serious issues that can happen with the misuse of generators.

If you own an older portable generator and want to reduce your risk of carbon monoxide even more, it might be time to invest in a new one. According to Consumer Reports, a handful of new portable generators provide a built-in sensor that activates an automatic shutoff if CO builds up to a dangerous level in an enclosed space. This may be your best option if you want to ensure a safe space for you and your family. Generator Safety Tips - Consumer Reports |

Contact Us(936) 327-4364 Archives

March 2024

Categories

All

|

Navigation |

Connect With Us

Share This Page |

Contact UsFirst Community Financial Group, Inc.

115 W. Polk St. Livingston, TX 77351 (936) 327-4364 Click Here to Email Us |

Location

|

RSS Feed

RSS Feed